On the desk of a mid-sized accounting firm in the United States, the landscape remains stubbornly analog. Thousands of pages of tax code documents sit beside aging Excel spreadsheets, reflecting a reality shared by 46,000 small-scale firms across the country. These long-tail practitioners lack the technical infrastructure to build proprietary AI models and view technology not as an asset to be owned, but as a utility to be purchased. For these firms, the value of AI is not found in a sophisticated chat interface, but in the ability to eliminate the manual drudgery that defines their workday.

The Architecture of Workflow Grit

This fragmented market is where vertical AI is finding its most aggressive growth. Blue J, an AI-driven tax research platform, currently serves over 2,800 organizations and has seen its usage surge by 700% over the past year. The scale of the opportunity is immense, as the US tax market is valued at 145 billion dollars, with 86% of that market comprised of small firms. These entities operate in a high-stakes environment where a single error in tax interpretation can lead to significant liabilities, making the precision of a verticalized tool more valuable than the general intelligence of a frontier model.

Similar dynamics are playing out in the debt collection sector through Salient, an AI agent designed for automotive loan recovery. Salient does not simply generate text; it operates within a rigid regulatory framework governed by the Fair Debt Collection Practices Act (FDCPA), the Telephone Consumer Protection Act (TCPA), and Regulation F. In this space, the cost of a human collection agent ranges from 4 to 12 dollars per call. By automating these interactions while maintaining strict legal compliance, the AI drastically reduces the cost per acquisition of recovered funds.

In healthcare, Charta Health is tackling the complexity of insurance claim chart reviews. The system must navigate a labyrinth of regional insurance rules and Current Procedural Terminology (CPT) codes, where the nuance of a specific medical code determines whether a claim is paid or denied. Meanwhile, the logistics sector is seeing a coordinated assault from HappyRobot, Pallet, and Augment. These tools are targeting a logistics operations market with annual costs totaling 1 trillion dollars, focusing on the coordination and optimization of freight and warehouse movements that have historically relied on manual emails and phone calls.

From Software Subscription to Labor Replacement

For years, the AI industry measured value through the lens of the software subscription. The goal was to capture a slice of the software budget, which is typically a small, guarded portion of a company's operational expenditure. However, a fundamental shift is occurring where vertical AI companies are redefining their Total Addressable Market (TAM) by targeting the labor budget instead of the software budget. This shift represents a move from providing a tool that helps a human work faster to providing a system that performs the work itself.

Consider the economics of a real estate management company. A traditional software-as-a-service (SaaS) approach would target the 30,000 dollars the company spends annually on leasing software. A vertical AI approach, however, targets the 300,000 dollars spent on the salaries of leasing agents. By shifting the target from the software budget to the labor budget, the potential revenue per customer expands by 30 times. EliseAI has executed this strategy with precision, starting with a single SKU for leasing automation and successfully penetrating one out of every eight apartments in the United States.

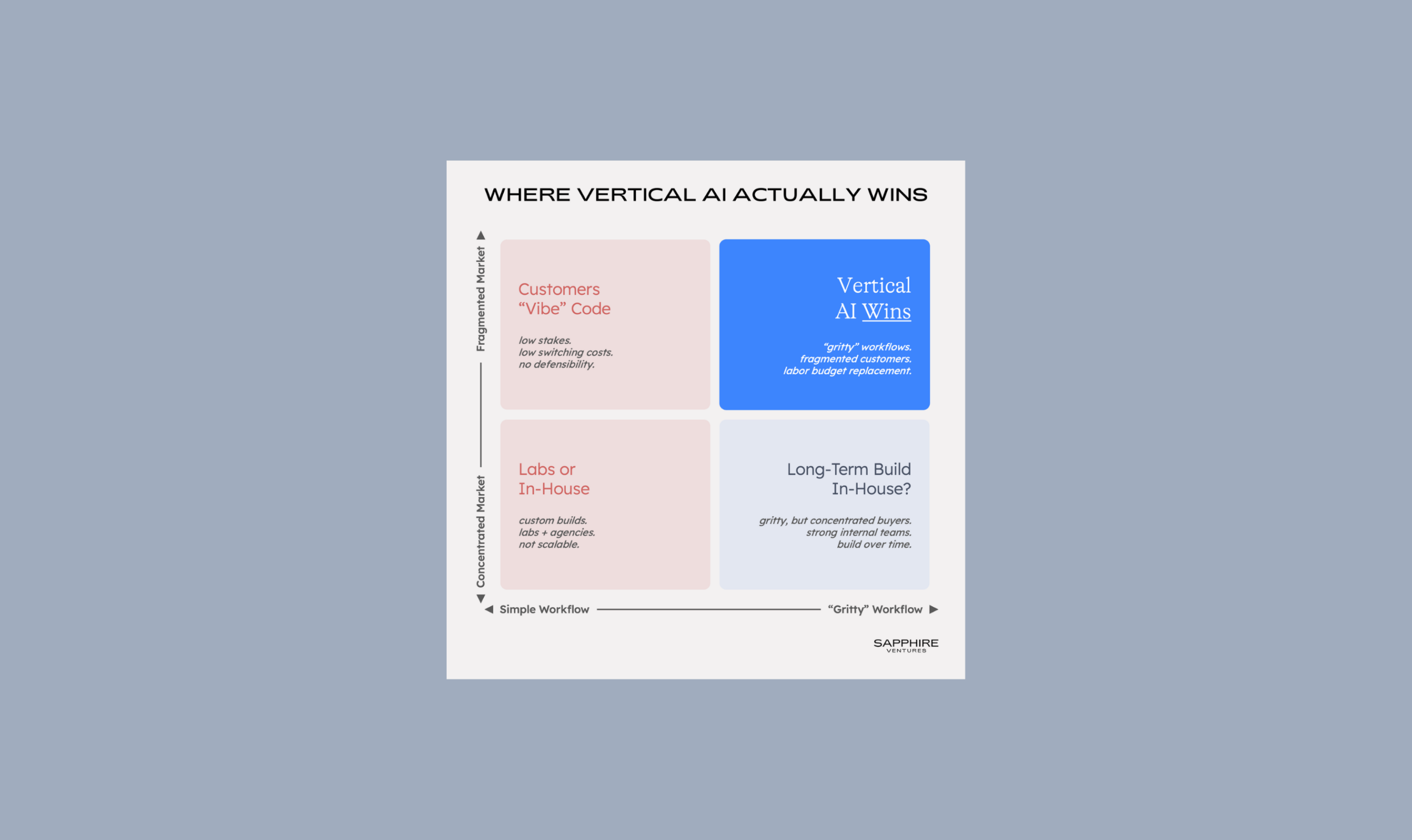

This strategy creates a defensive moat that frontier labs like OpenAI or Anthropic are poorly positioned to cross. While frontier labs focus on increasing the raw intelligence of the model, they generally avoid the operational complexity of specific industries. Vertical AI firms embrace this complexity, which can be described as workflow grit. Workflow grit is the combination of unstructured data, legacy system integration, and the necessity of regulatory approval loops. The higher the workflow grit, the harder it is for a competitor to replicate the functionality simply by updating a model.

When a frontier lab releases a more powerful model, it may win the demo, but the vertical AI system wins the market. This is because the vertical system has already integrated itself into the distribution channels and accumulated a compound interest of operational context. The model is the engine, but the workflow is the vehicle. As model performance begins to plateau across the industry, the competitive advantage shifts away from the algorithm and toward the entity that controls the messy, real-world processes of the job site.

The victory in the AI era will not belong to the most intelligent model, but to the system that most effectively absorbs the cost of human labor.