For years, the ritual of AI-driven financial planning has been a tedious exercise in manual labor. Users would export CSV files from their banking portals, scrub sensitive account numbers, and upload PDFs of monthly statements, hoping the LLM could spot a spending leak or categorize a rogue subscription. It was a fragmented workflow that treated the AI as a static calculator rather than a dynamic assistant. This week, that friction vanished as OpenAI moved the AI directly into the financial stream.

The Plaid Integration and the Pro Paywall

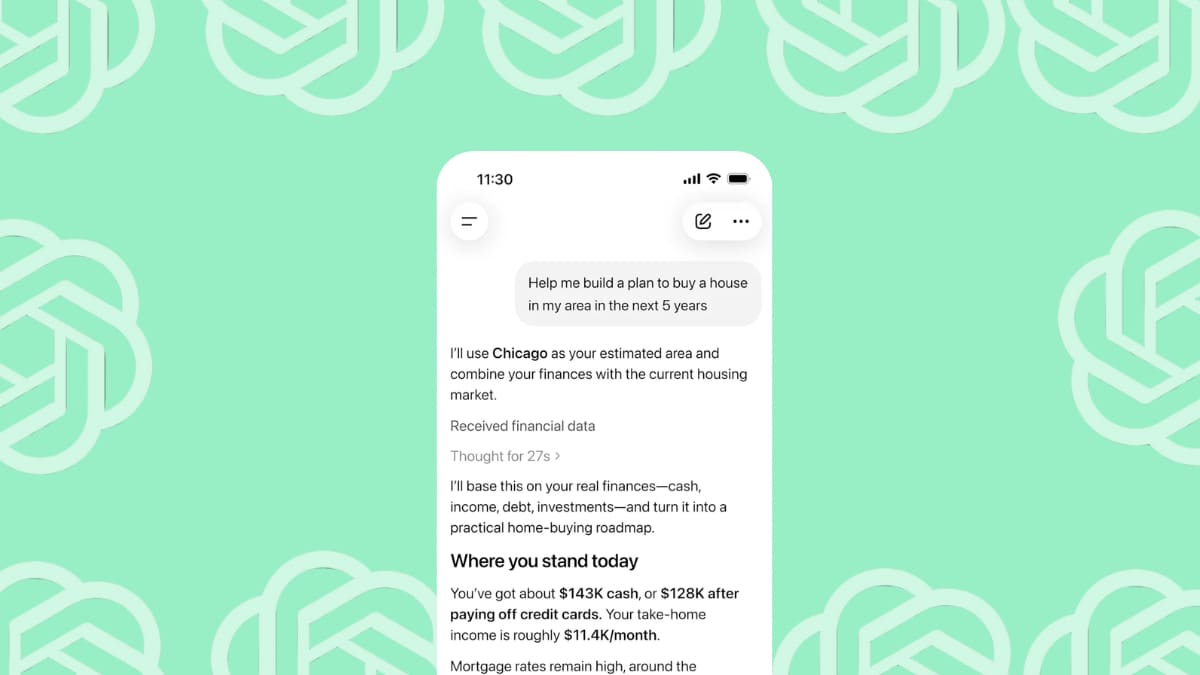

OpenAI has officially integrated ChatGPT with Plaid, the industry-standard middleware that bridges the gap between financial institutions and third-party applications. This connection allows ChatGPT to pull live data from over 12,000 financial institutions, including heavyweights like Chase, Fidelity, Capital One, and Schwab. The scope of access is comprehensive. Once linked, ChatGPT can monitor real-time account balances, parse detailed transaction histories, identify active subscription services, and track investment portfolios. It also gains visibility into the user's liabilities, including mortgage balances and credit card debt.

This data flow transforms the chatbot into a personalized financial controller. Users now receive visualized spending dashboards and tailored financial advice based on their actual liquidity and debt ratios. The system is also designed to act as a proactive sentinel, triggering alerts when the AI detects spending patterns that deviate from the user's established norm. However, this level of intimacy comes with a steep entry price. The feature is currently in a preview phase, available exclusively to Pro subscribers paying $200 per month. OpenAI intends to roll the functionality out to Plus subscribers and general users in subsequent phases.

The Gap Between Control and Sovereignty

The shift from static file uploads to real-time data streams fundamentally changes the power dynamic between the user and the model. While OpenAI emphasizes that the AI cannot modify account details or access full account numbers, a critical gap exists in the data lifecycle. Users can disconnect their accounts and request the deletion of their financial memory, but the system requires up to 30 days to fully purge that data. This latency creates a window where the user's perceived deletion does not align with the system's actual state.

More telling is the psychological framing used during the data consent process. When asking users to share their financial data for model training, OpenAI employs a nudge, labeling the option as an opportunity to improve the model for everyone. This phrasing shifts the narrative from a corporate data acquisition play to a communal contribution, masking the fact that highly sensitive financial signals are being used to refine a proprietary commercial product.

This strategy mirrors the launch of ChatGPT Health in January, which allowed users to link medical records for health-related queries. In that instance, OpenAI distanced itself from diagnostic claims but remained vague on the specifics of data protection and breach response. The Plaid integration follows the same playbook: offering granular user controls while remaining opaque about how this financial intelligence might be commercialized beyond model training.

When an AI can track millions of users' income signals, debt levels, and spending habits in real-time, it is no longer just a chatbot; it is a massive, living dataset of consumer behavior. By combining this data with the reasoning capabilities of an LLM, OpenAI is building a comprehensive financial profile of its user base. For a company under immense pressure to find sustainable revenue streams, this infrastructure is a goldmine. The leap from a spending dashboard to personalized financial product recommendations or proprietary credit scoring models is a short one. The risk is that as the corporate structure of OpenAI evolves, the guardrails protecting this intimate data may shift to accommodate new business models.

Convenience is the hook, but the true cost of a real-time financial AI is the gradual surrender of data sovereignty.